SIP ₹2000 Per Month: How Much Will You Get in 3, 5, 10, 15, 20 & 30 Years?

₹2000 a month — less than most people spend on subscriptions. Yet invested consistently in a SIP, it builds serious wealth over time. Here are the exact numbers across every timeframe so you know precisely what ₹2000/month is worth.

- 1. Is ₹2000 a Month a Good Amount to Invest?

- 2. Exact Returns: ₹2000/Month for 3, 5, 10, 15, 20 & 30 Years

- 3. Returns at Different Interest Rates

- 4. Global Equivalent — $2000/Month Investment Returns

- 5. ₹2000 SIP Returns by Country & Currency

- 6. What If You Step Up ₹2000 by 10% Every Year?

- 7. Where to Invest ₹2000 Per Month

- 8. ₹2000 vs ₹1000 vs ₹500 SIP — Full Comparison

- 9. How to Start ₹2000 SIP Today

- 10. Frequently Asked Questions

1. Is ₹2000 a Month a Good Amount to Invest?

Absolutely. ₹2000/month is one of the most effective SIP amounts for working professionals in India. It is affordable enough to sustain long-term, yet powerful enough to build a corpus that crosses ₹20 lakh in 20 years and ₹70 lakh in 30 years with step-up.

Most people who start with ₹2000/month and enable a 10% annual step-up end up crossing ₹1 crore well within their working years — without ever feeling the pinch of investing.

Key Insight: ₹2000/month at 12% for 30 years = ₹70.4 lakh. Your total investment is just ₹7.2 lakh. The remaining ₹63.2 lakh is pure compounding — nearly 9x your money from just ₹2000/month.

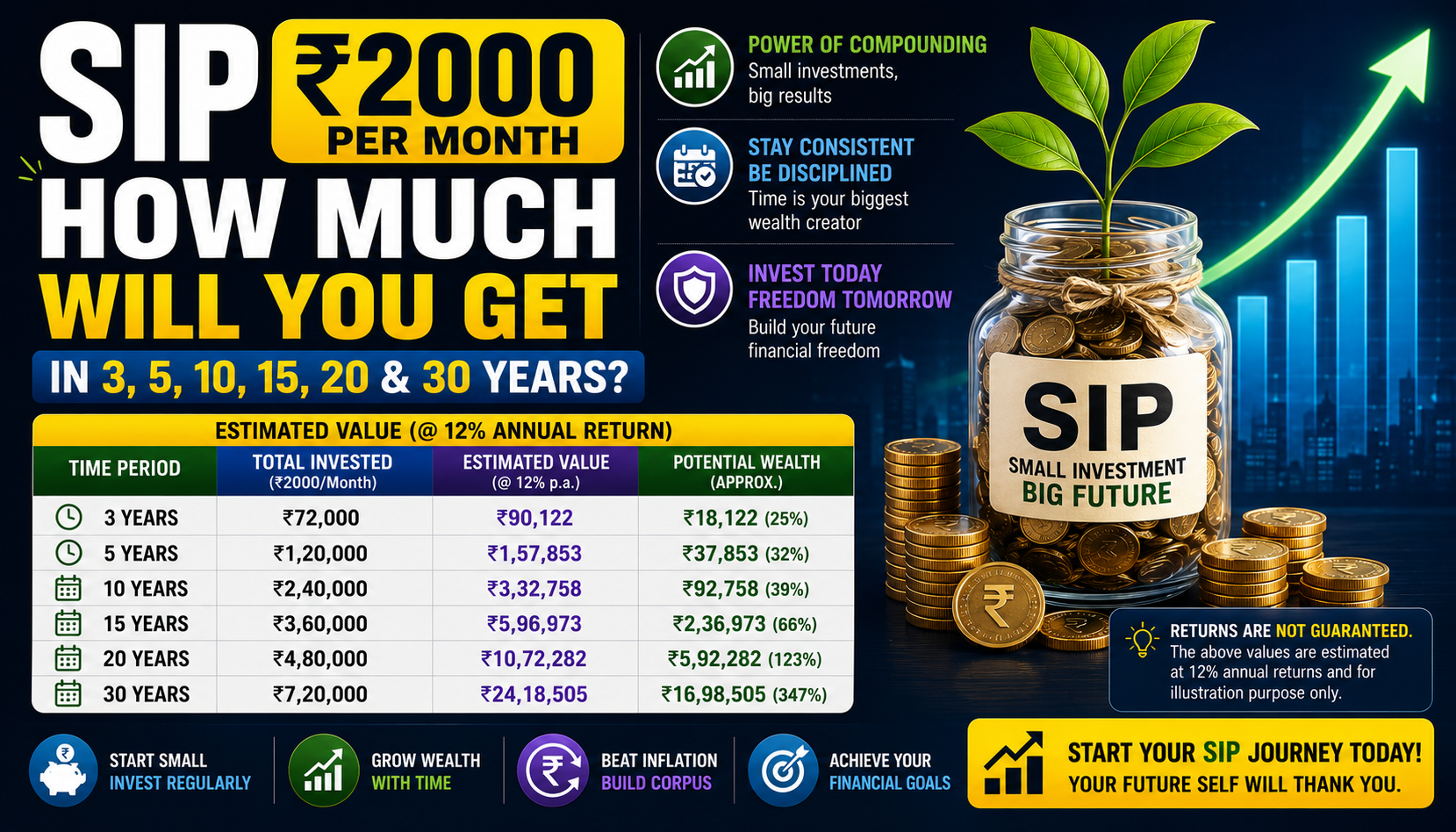

2. Exact Returns: ₹2000/Month for All Timeframes

All calculations below assume 12% annual return — the historical average of diversified equity mutual funds in India.

| Timeframe | Total Invested | Est. Returns | Total Corpus |

|---|---|---|---|

| 3 Years | ₹72,000 | ₹13,952 | ₹85,952 |

| 5 Years | ₹1.20 Lakh | ₹44,880 | ₹1.65 Lakh |

| 10 Years | ₹2.40 Lakh | ₹2.24 Lakh | ₹4.64 Lakh |

| 15 Years | ₹3.60 Lakh | ₹6.44 Lakh | ₹10.04 Lakh |

| 20 Years | ₹4.80 Lakh | ₹15.18 Lakh | ₹19.98 Lakh |

| 25 Years | ₹6.00 Lakh | ₹32.64 Lakh | ₹38.64 Lakh |

| 30 Years | ₹7.20 Lakh | ₹63.2 Lakh | ₹70.4 Lakh |

Notice this: You invest ₹7.20 lakh over 30 years but get back ₹70.4 lakh. That's nearly 10x your money — from just ₹2000/month. This is the magic of long-term compounding.

3. Returns at Different Interest Rates

Here's how ₹2000/month grows over 20 years at different return rates:

| Annual Return | 20-Year Corpus | Typical Fund Type |

|---|---|---|

| 6% | ₹9.28 Lakh | Fixed Deposit / PPF |

| 8% | ₹11.80 Lakh | Balanced / Hybrid Fund |

| 10% | ₹15.20 Lakh | Large Cap Fund |

| 12% | ₹19.98 Lakh | Diversified Equity Fund |

| 14% | ₹26.20 Lakh | Mid / Small Cap Fund |

| 16% | ₹34.52 Lakh | Small Cap / Sectoral Fund |

Recommendation: Use 10–12% as your planning return rate. Conservative planning ensures you reach your goal even in moderate market conditions.

4. Global Equivalent — $2000/Month Investment Returns

For global investors putting away $2000/month in index funds at 10% annual return:

| Timeframe | Total Invested | Est. Returns | Total Corpus |

|---|---|---|---|

| 3 Years | $72,000 | $11,856 | $83,856 |

| 5 Years | $1,20,000 | $32,328 | $1,52,328 |

| 10 Years | $2,40,000 | $1,68,000 | $4,08,000 |

| 20 Years | $4,80,000 | $10,28,000 | $15,08,000 |

| 25 Years | $6,00,000 | $20,64,000 | $26,64,000 |

| 30 Years | $7,20,000 | $37,88,000 | $45,08,000 |

Global Insight: $2000/month for 30 years at 10% = over $4.5 million. You invest $720,000 and retire a multi-millionaire — purely from $2000/month consistency.

5. ₹2000 SIP Returns by Country & Currency

The equivalent of ₹2000/month in other currencies, and what it grows to in 20 years at 10% return:

6. What If You Step Up ₹2000 by 10% Every Year?

Step-up SIP means increasing your monthly investment by 10% every year automatically. Here's the dramatic impact on your final wealth:

| Timeframe | Flat ₹2000/mo | 10% Step-Up | Extra Wealth |

|---|---|---|---|

| 10 Years | ₹4.64 Lakh | ₹6.96 Lakh | +₹2.32 Lakh |

| 15 Years | ₹10.04 Lakh | ₹18.24 Lakh | +₹8.20 Lakh |

| 20 Years | ₹19.98 Lakh | ₹43.36 Lakh | +₹23.38 Lakh |

| 30 Years | ₹70.4 Lakh | ₹2.52 Crore | +₹1.82 Crore |

Powerful: A 10% annual step-up turns ₹70.4 lakh into ₹2.52 crore over 30 years — from the same ₹2000 starting point. That's 3.6x more wealth for increasing by just ₹200 in year two.

See Your Exact ₹2000 SIP Returns Instantly

Use our free calculator — enter your amount, rate & years. Get results in seconds.

7. Where to Invest ₹2000 Per Month

- Groww — Zero commission, ₹100 minimum SIP, best for beginners

- INDmoney — Supports both Indian SIP and US stock investing from one app

- Zerodha Coin — Direct mutual fund plans, lowest expense ratios

- Paytm Money — Simple interface, great for first-time investors

- MF Central — Official AMFI platform, completely free

- USA: Fidelity or Vanguard — S&P 500 index fund, $1 minimum

- UK: Vanguard UK or Hargreaves Lansdown — Stocks & Shares ISA

- UAE: Sarwa or Wahed Invest — Halal options available

- Singapore: Syfe or StashAway — automated monthly investing

- Europe: Trade Republic or Scalable Capital — MSCI World ETF

8. ₹2000 vs ₹1000 vs ₹500 SIP — Full Comparison

Here is a direct side-by-side comparison of all three amounts at 12% annual return:

| Timeframe | ₹500/Month | ₹1000/Month | ₹2000/Month |

|---|---|---|---|

| 5 Years | ₹41,220 | ₹82,440 | ₹1.65 Lakh |

| 10 Years | ₹1.16 Lakh | ₹2.32 Lakh | ₹4.64 Lakh |

| 20 Years | ₹4.99 Lakh | ₹9.99 Lakh | ₹19.98 Lakh |

| 30 Years | ₹17.6 Lakh | ₹35.2 Lakh | ₹70.4 Lakh |

Simple Truth: Every time you double your SIP amount, your final corpus doubles too. If ₹2000/month is affordable — start with ₹2000. If not — start with ₹500 today and upgrade as your income grows.

9. How to Start ₹2000 SIP Today

Complete Your KYC

Complete a one-time KYC on Groww, INDmoney or Zerodha Coin using your Aadhaar and PAN. Takes under 5 minutes.

Choose a Fund

For beginners: Nifty 50 Index Fund (direct plan). For slightly higher returns: Flexicap or Multi-cap Fund (direct plan).

Set SIP at ₹2000/Month

Select monthly SIP, enter ₹2000, pick your date (1st or 5th of the month works well), and confirm.

Enable Step-Up at 10%

Most platforms let you enable annual step-up when creating the SIP. Turn this on — your ₹2000 becomes ₹3,221 in 5 years automatically.

Set Up Auto-Debit & Forget

Authorize NACH mandate so ₹2000 is auto-debited every month. Then stop watching it daily. Let time do the work.

10. Frequently Asked Questions

How much will ₹2000 per month SIP give in 10 years?

At 12% annual return, ₹2000/month SIP for 10 years gives a corpus of approximately ₹4.64 lakh. Total invested: ₹2.40 lakh. Returns earned: ₹2.24 lakh.

How much will ₹2000 per month SIP give in 20 years?

At 12% annual return, ₹2000/month SIP for 20 years gives a corpus of approximately ₹19.98 lakh. Total invested: ₹4.80 lakh — the remaining ₹15.18 lakh is pure compounding.

Is ₹2000 per month SIP enough to become a millionaire?

Yes. With a 10% annual step-up starting at ₹2000/month, you can reach ₹1 crore in approximately 22 years at 12% return. Without step-up, flat ₹2000/month at 12% for 30 years = ₹70.4 lakh.

Which fund is best for ₹2000 per month SIP?

For a 15–20 year horizon, Nifty 50 Index Fund (direct plan) is the most reliable choice. For higher potential returns with moderate risk, consider Flexicap or Multi-cap funds in direct plans.

Should I invest ₹2000 in one fund or split it?

At ₹2000/month, investing in one good diversified fund is better than splitting. Splitting ₹2000 into two ₹1000 SIPs adds complexity without meaningful diversification. Once your SIP crosses ₹5000/month, splitting across 2 funds makes more sense.

What is the difference between ₹1000 and ₹2000 SIP over 20 years?

At 12% return over 20 years: ₹1000/month = ₹9.99 lakh, ₹2000/month = ₹19.98 lakh. The difference is exactly ₹9.99 lakh — doubling your SIP doubles your corpus every time.

Can I increase my SIP from ₹2000 to a higher amount later?

Yes, absolutely. You can either enable the step-up feature for automatic annual increases, or manually start a new SIP for the additional amount. Both methods work well and most platforms support them easily.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. All corpus projections are based on assumed return rates and actual returns may vary significantly. Investment in mutual funds is subject to market risks. Past performance is not indicative of future results. Consult a SEBI-registered investment advisor before making any investment decisions.