Inflation Impact on SIP Returns: How Inflation Silently Erodes Your Wealth

Most SIP calculators show you impressive numbers. "₹1 crore in 20 years!" But there's a catch nobody tells you: that ₹1 crore won't buy in 20 years what it can buy today. Inflation is the silent thief of wealth — and understanding it is the difference between planning with illusions and planning with reality.

- 1. What is Inflation and Why Does It Matter?

- 2. Nominal Returns vs Real Returns

- 3. The Real Return Formula

- 4. How Inflation Destroys Purchasing Power

- 5. The Shocking Real Numbers

- 6. Inflation Impact by Asset Class

- 7. Global Inflation Rates & SIP Impact

- 8. How to Beat Inflation with SIP

- 9. Inflation-Adjusted Goal Planning

- 10. Use Our Inflation-Adjusted Calculator

- 11. Frequently Asked Questions

1. What is Inflation and Why Does It Matter for SIP Investors?

Inflation is the rate at which the general price level of goods and services rises over time. When inflation is 6%, something that costs ₹100 today will cost ₹106 next year. This seems small — but over 20 years at 6% inflation, that ₹100 item costs ₹321.

For SIP investors, inflation matters because your financial goals are not about accumulating a number — they're about buying something with that number. Whether it's your child's education, retirement income, or buying a house, all those goals will cost significantly more in the future than they do today.

The Real Problem: Most investors celebrate when their SIP reaches ₹1 crore. But at 6% annual inflation, ₹1 crore in 20 years has the purchasing power of just ₹31 lakh today. Are you planning for ₹1 crore or ₹31 lakh worth of goals?

India's long-term average inflation has been 5–6% annually based on RBI data. Education inflation runs at 10–12%, healthcare at 8–10%, and general consumer inflation at 5–6%. This means your SIP goals must account for these different inflation rates depending on what you're saving for.

2. Nominal Returns vs Real Returns — The Critical Difference

This is the most important concept for every SIP investor to understand:

- Nominal Return — the raw percentage your investment grows. This is what fund advertisements show you.

- Real Return — your nominal return adjusted for inflation. This is what actually matters.

A 12% nominal return sounds great. But if inflation is 6%, your real return is only about 5.66% — not 6% as many people mistakenly think (more on the exact formula below).

| Scenario | Nominal Return | Inflation | Real Return | Verdict |

|---|---|---|---|---|

| Equity SIP (Best Case) | 14% | 6% | 7.55% | Beats inflation ✅ |

| Equity SIP (Average) | 12% | 6% | 5.66% | Beats inflation ✅ |

| Hybrid Fund | 9% | 6% | 2.83% | Barely beats ⚠️ |

| Debt Fund | 7% | 6% | 0.94% | Barely beats ⚠️ |

| Fixed Deposit | 6.5% | 6% | 0.47% | Barely survives ❌ |

| Savings Account | 3.5% | 6% | -2.36% | Loses money ❌ |

3. The Real Return Formula — The Fisher Equation

Many people calculate real returns by simply subtracting inflation from nominal returns. This is an approximation. The accurate formula (known as the Fisher Equation) is:

Example: Nominal = 12%, Inflation = 6% → Real Return = (1.12 ÷ 1.06) − 1 = 5.66% (not 6%)

The simple subtraction method (12% − 6% = 6%) overestimates your real return. The Fisher Equation is more accurate and becomes increasingly important over longer time periods and higher inflation rates.

Our SIP Calculator uses the accurate Fisher Equation formula to show you both nominal and inflation-adjusted real values side by side. Enter your inflation rate and see the real picture instantly.

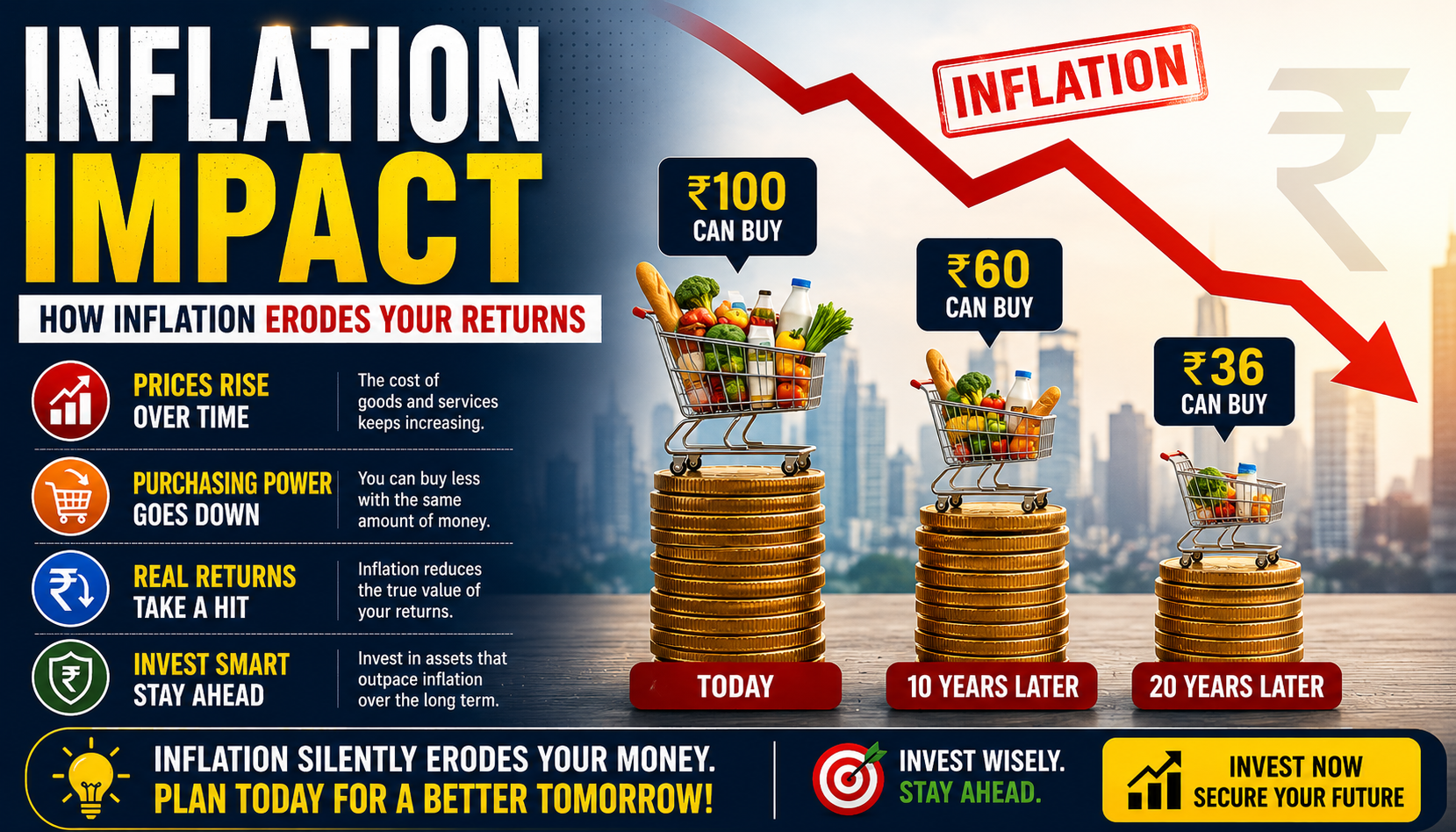

4. How Inflation Destroys Purchasing Power Over Time

The most visceral way to understand inflation is through purchasing power. At 6% annual inflation, ₹100 today can buy progressively fewer goods over time:

This is why the Rule of 72 applies to inflation too: At 6% inflation, purchasing power halves every 12 years (72 ÷ 6 = 12). Your ₹1 crore corpus in 2046 will only buy what ₹31 lakh buys today if inflation averages 6%.

Goal Inflation: If your child's education costs ₹20 lakh today and education inflation is 10%, it will cost ₹1.34 crore in 20 years. Planning for ₹20 lakh today and expecting it to be enough in 2046 is a catastrophic miscalculation.

5. The Shocking Real Numbers — What Your SIP Really Earns

Let's look at a ₹10,000/month SIP at 12% nominal return over 20 years, with 6% inflation:

Your nominal corpus of ₹1 crore has a real purchasing power of just ₹31 lakh in today's money — after 20 years of 6% inflation

| Duration | Nominal Corpus | Real Value (Today's ₹) | Loss to Inflation |

|---|---|---|---|

| 10 Years | ₹23.23 L | ₹12.98 L | -₹10.25 L |

| 15 Years | ₹50.46 L | ₹21.05 L | -₹29.41 L |

| 20 Years | ₹1.00 Cr | ₹31.18 L | -₹68.82 L |

| 30 Years | ₹3.53 Cr | ₹61.40 L | -₹2.92 Cr |

The numbers are sobering. But here's the critical point: equity SIPs still beat inflation. A real return of 5.66% over 30 years still grows your money significantly. The problem is when investors don't plan for inflation and set their goals based on nominal figures alone.

6. Inflation Impact by Asset Class

Not all investments are equally affected by inflation. Here's how different asset classes fare:

- Equity Mutual Funds (SIP): Best inflation beater. Historical returns of 12–14% in India vs 5–6% inflation = 6–8% real return. Best for goals 10+ years away.

- Gold: Good inflation hedge historically. Avg 8–10% long-term returns. Best used as 10–15% portfolio allocation, not primary investment.

- Hybrid/Balanced Funds: Returns of 8–10%. Marginally beats inflation. Suitable for medium-term goals (5–10 years).

- Debt Mutual Funds: Returns of 6–8%. Barely beats or matches inflation. Suitable for short-term goals (1–3 years).

- Fixed Deposits: Returns of 6–7%. After tax, often cannot beat inflation. Loses real value over time.

- Savings Account: Returns of 3–4%. Significantly below inflation. Money loses purchasing power rapidly.

- Cash under the mattress: 0% return. Loses purchasing power at 100% of the inflation rate. Never hold idle cash long-term.

7. Global Inflation Rates & Their Impact on SIP Investors

Inflation rates vary significantly across countries, which affects how much real return investors need to target:

| Country | Avg Inflation | Target Nominal Return | Best Instruments |

|---|---|---|---|

| India | 5–6% per year | 12%+ (equity) | Equity mutual funds via SIP |

| USA | 3–4% per year | 8–10% (index funds) | S&P 500 index ETFs via DCA |

| Europe (EU) | 3–5% per year | 8–10% | MSCI World ETFs, Trade Republic |

| UK | 3–4% per year | 8–10% | ISA accounts, FTSE index funds |

| Middle East | 2–4% per year | 7–9% | Global ETFs, Halal funds (Wahed) |

8. How to Beat Inflation with SIP — 6 Proven Strategies

Choose Equity Funds for Long-Term Goals

Equity mutual funds are the most proven inflation beaters over 10+ year periods. NSE data shows equity delivered 12–14% average annual returns over 30+ years in India — well above 5–6% inflation. Debt funds and FDs cannot beat inflation meaningfully after tax.

Use Step-Up SIP to Match Inflation

Increase your SIP by at least the inflation rate every year. If inflation is 6% and you want real wealth growth, increase your SIP by 10–12% annually. This ensures your investment amount doesn't lose real value over time.

Plan Goals in Today's Rupees, Then Add Inflation

If you need ₹50 lakh for your child's education in 15 years and education inflation is 10%, your actual target is ₹2.09 crore in nominal terms. Always inflate your goals before calculating your required SIP amount.

Minimize Expense Ratios

Every 1% saved on expense ratio is 1% more real return. Choose direct plans over regular plans. At 12% nominal return, switching from a 1.5% expense ratio fund to a 0.5% direct plan increases your real return from 4.24% to 5.17% — a 22% improvement in real terms.

Stay Invested — Never Stop During High Inflation

High inflation periods are often accompanied by rising interest rates and volatile markets. This is exactly when most investors stop their SIP — and make the biggest mistake. Staying invested during volatility is what separates wealthy investors from average ones.

Add Inflation Hedges to Your Portfolio

Allocate 10–15% to gold ETFs or gold mutual funds as an inflation hedge. Real estate REITs can also be an inflation hedge. These assets tend to maintain or increase their value during high inflation periods.

See Your Real Inflation-Adjusted Returns

Our SIP calculator shows both nominal and inflation-adjusted values side by side. Set your inflation rate and see the real picture.

9. Inflation-Adjusted Goal Planning — The Right Way

Most people set financial goals in today's money and forget to inflate them. Here's the correct approach for common life goals:

| Goal | Today's Cost | Inflation Rate | Years Away | Future Cost |

|---|---|---|---|---|

| Child's Education | ₹20 L | 10% | 15 yrs | ₹83.5 L |

| Child's Wedding | ₹25 L | 8% | 20 yrs | ₹1.17 Cr |

| Retirement Corpus | ₹1 Cr | 6% | 25 yrs | ₹4.29 Cr |

| House Down Payment | ₹30 L | 8% | 10 yrs | ₹64.8 L |

The takeaway: always plan your SIP target based on the future inflated cost of your goal, not today's cost. Under-saving is the biggest risk of ignoring inflation in goal planning.

10. Use Our Inflation-Adjusted SIP Calculator

Our free SIP calculator at SipCalculatorPro.net is one of the very few calculators that shows you both nominal and real inflation-adjusted values simultaneously. Here's how to use it for inflation-aware planning:

- Set your monthly SIP amount

- Enter your expected return (12% for equity, 8% for balanced, 6% for debt)

- Set your investment duration (match your goal timeline)

- Set the Inflation Rate — use 6% for general goals, 10% for education, 8% for healthcare

- The calculator shows you both the nominal corpus AND the real value in today's money

- If the real value doesn't meet your goal, increase the SIP amount or duration

Pro Tip: Our calculator supports 15 currencies. Whether you're in India (₹), USA ($), Europe (€), or the Middle East (AED), you can calculate your inflation-adjusted SIP returns in your own currency. Try it now →

11. Frequently Asked Questions

How does inflation affect SIP returns?

Inflation reduces the purchasing power of your SIP corpus. If your SIP earns 12% nominally and inflation is 6%, your real return is only 5.66% using the Fisher Equation. This means your money grows nominally but buys less than the headline figure suggests. Our calculator shows both figures side by side.

What is the real return formula for SIP?

The accurate formula is: Real Return = ((1 + Nominal Return) / (1 + Inflation Rate)) - 1. For a 12% nominal return with 6% inflation: (1.12 / 1.06) - 1 = 5.66% real return. Simply subtracting inflation (12% - 6% = 6%) is an approximation that overestimates real returns.

Can SIP beat inflation?

Yes — equity SIPs have historically beaten inflation in India with 12–14% average annual returns vs 5–6% average inflation. According to NSE data, equity has delivered 12–14% average returns over 30+ years. Over 10+ year periods, equity SIPs have consistently delivered positive real returns.

Which mutual fund type best beats inflation?

Equity mutual funds — particularly large-cap index funds, flexicap funds, and multi-cap funds — have historically been the best inflation beaters. Debt funds and FDs often fail to beat inflation after tax in high-inflation environments.

How much should I increase my SIP to beat inflation?

Increase your SIP by at least the inflation rate each year. If inflation is 6% and you want real wealth growth, increase your SIP by 10–12% annually. This is exactly what Step-Up SIP does automatically — it keeps your investment growing in real terms, not just nominal terms.

What inflation rate should I use in the SIP calculator?

Use 6% for general financial goals in India. Use 10–12% for education goals. Use 8–10% for healthcare goals. For global investors: 3–4% for USA/UK/Europe, 2–4% for Middle East. Always be conservative — planning for higher inflation and being surprised by lower inflation is better than the reverse.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. Investment in mutual funds is subject to market risks. Inflation projections are estimates based on historical data and may not predict future inflation rates. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future results. Consult a SEBI-registered investment advisor before making any investment decisions.